The financial services industry (FSI) is undergoing a rapid digital transformation, with credit card payment processing platforms playing a central role. As societies move toward cashless ecosystems and businesses expand globally, there is a rising demand for secure, scalable, and resilient payment infrastructures.

Amazon Web Services (AWS) provides a robust set of tools to help organizations develop and maintain modern credit card processing systems. In this article, we’ll guide you through the key components and considerations of building a cloud-native credit card payment platform using AWS, focusing on the authorization process, security best practices, and reference architectures for both acquirers and issuers.

Why Choose AWS for Credit Card Payment Processing?

Before diving into the technicalities, it’s important to understand why AWS is the platform of choice for financial institutions and fintechs when it comes to payment processing:

Benefits of AWS for Payment Processing

- Elastic Scalability: Scale seamlessly during peak periods such as Black Friday or year-end sales events.

- High Availability: Maintain 24/7 uptime with minimal latency across thousands of transactions per second.

- Global Reach: Expand into new markets while complying with data residency and local regulatory requirements.

- Enhanced Security: Protect sensitive data using AWS’s multi-layered security infrastructure, including encryption, IAM, and threat detection.

- Innovation-Friendly: Accelerate time-to-market for new features through DevOps, containerization, and infrastructure as code (IaC).

With AWS, businesses can modernize their legacy systems and build future-proof solutions that cater to rapidly evolving customer expectations.

Understanding Credit Card Processing: Key Steps & Players

Each credit card payment consists of three main stages:

- Authorization – Verifying the availability of funds and obtaining approval from the issuing bank.

- Clearing – Bundling authorized transactions for reconciliation.

- Settlement – Transferring funds to the merchant’s account.

To fully comprehend how these steps work on AWS, we first need to understand the main entities involved in a transaction.

Major Stakeholders in the Payment Lifecycle

- Merchants: Businesses that accept credit cards via terminals, eCommerce platforms, or apps.

- Payment Gateways: Act as intermediaries that securely transfer transaction data from merchants to processors.

- Payment Processors: Handle communication among stakeholders and provide value-added services.

- Acquirers (Merchant Banks): Provide merchant accounts, enabling businesses to accept card payments.

- Card Associations: Networks like Visa, Mastercard, and American Express that govern payment transactions.

- Issuing Banks: Issue credit cards and approve or decline transactions.

- Cardholders: Customers who initiate the transaction.

Each interaction must happen in milliseconds, and that’s where AWS tools come into play.

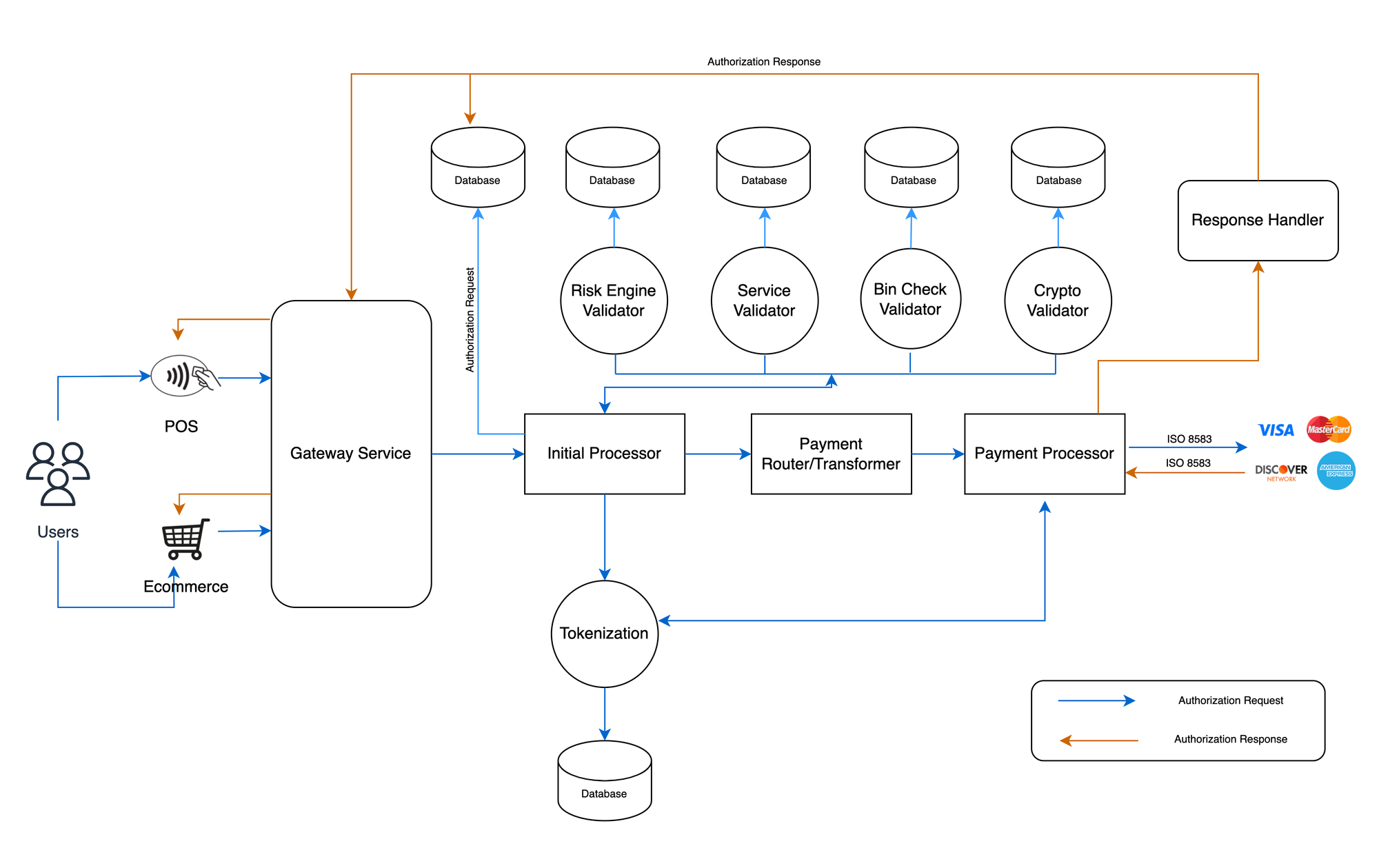

Step-by-Step: How Credit Card Authorization Works

Step 1: Cardholder Initiates Payment

The customer enters card details either in-person (card-present) or online (card-not-present). For online transactions, tokenization and encryption ensure that sensitive information isn’t stored by the merchant.

Step 2: Routing & Validation

The encrypted transaction data is sent to the payment gateway, which forwards it to a payment processor. Here, the Bank Identification Number (BIN) is used to determine:

- Which services (fraud check, account updater) should apply

- Which card network (Visa, Mastercard) to route the transaction to

Step 3: Card Network Processing

The card network de-tokenizes and enriches the transaction with on-behalf services like fraud detection and spend control.

Step 4: Issuer Authorization

The transaction is forwarded to the issuing bank or its processor, where various checks are run:

- Balance verification

- Fraud scoring

- Velocity and policy checks (e.g., daily spending limits)

- Address and chip verification

The issuer responds with an approval or decline message, which cascades back to the merchant terminal within seconds.

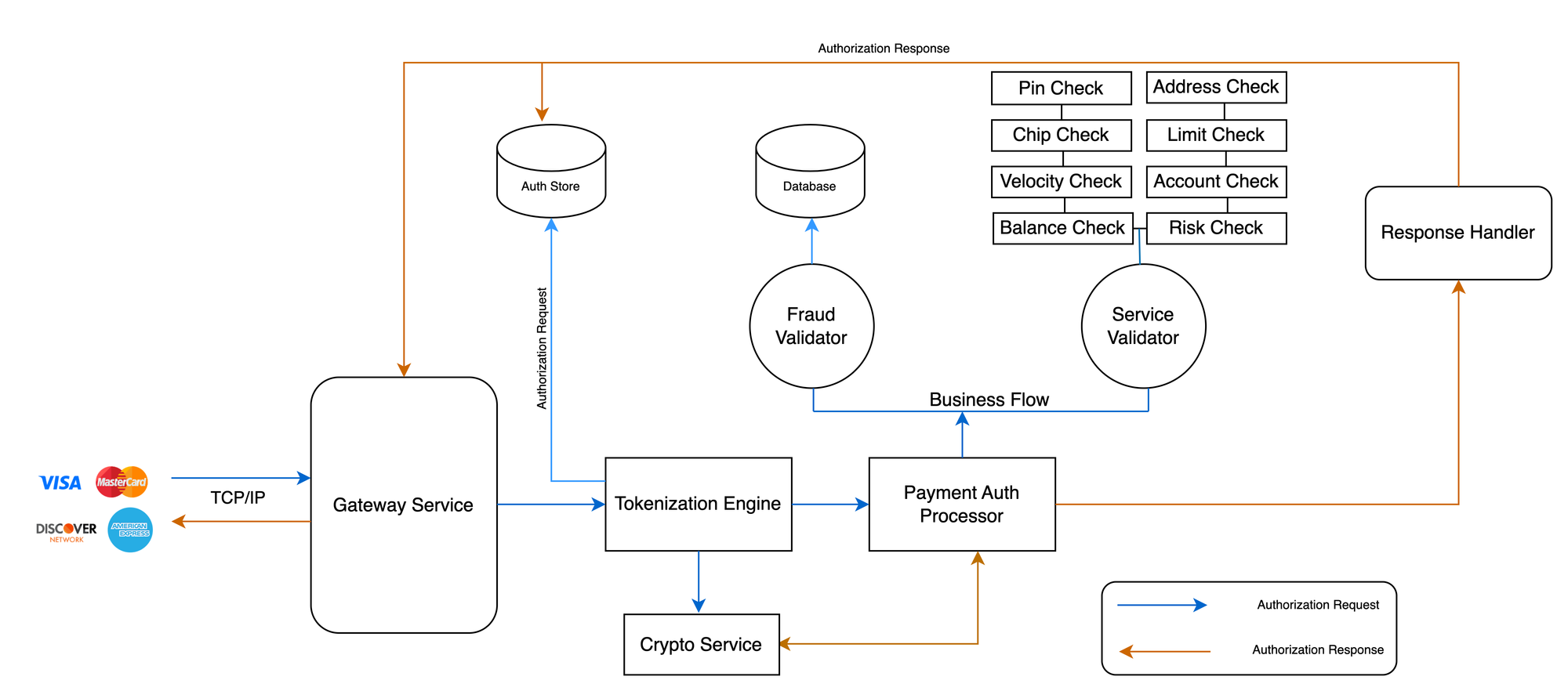

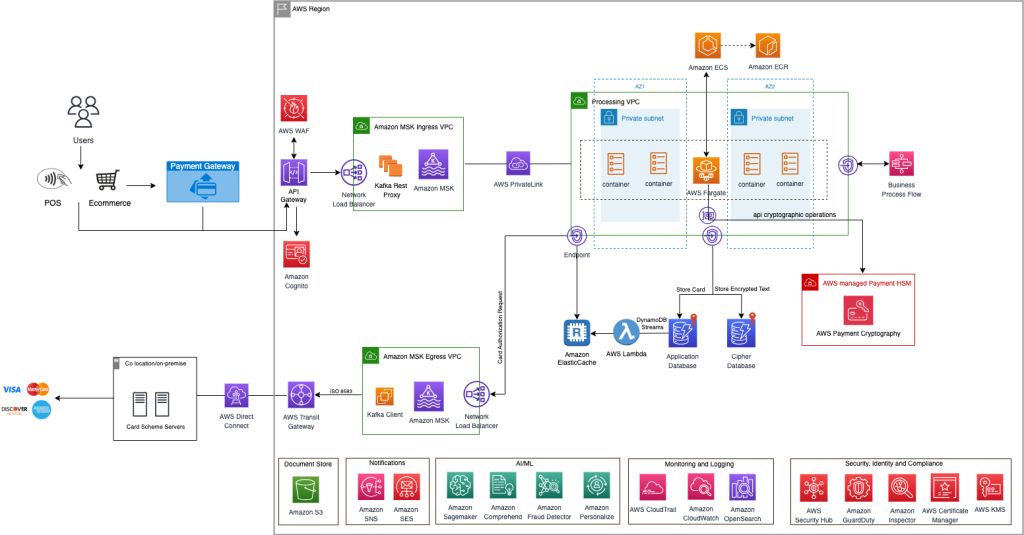

AWS Reference Architectures for Payment Authorization

AWS provides the infrastructure and services to support both acquiring and issuing sides of the transaction. Below, we detail the components of each architecture.

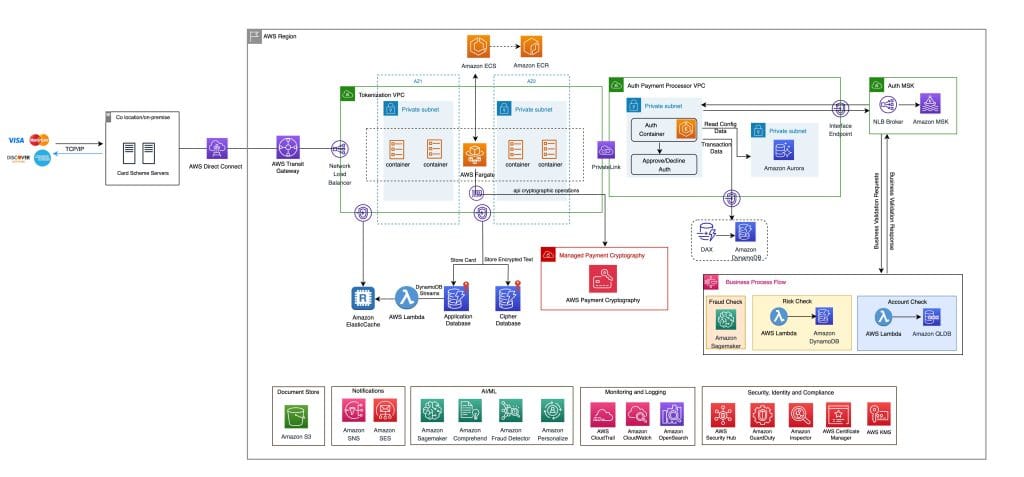

Acquiring Processor Architecture on AWS

- Amazon API Gateway: Receives encrypted card info through secure endpoints.

- AWS WAF & Amazon Cognito: Protect APIs from threats and ensure only authorized access.

- Amazon MSK (Kafka): Streams transaction events securely using TLS 1.3 and Secrets Manager.

- AWS Fargate (Containers): Scales container workloads without managing servers.

- AWS Payment Cryptography: Handles key cryptographic operations securely.

- Amazon DynamoDB: Stores application-specific metadata and token responses.

- Amazon ElastiCache for Redis: Offers ultra-fast in-memory storage for real-time validation.

- AWS Step Functions: Orchestrates risk, fraud, and account validation logic.

- Kafka Egress Stream: Sends formatted responses to card networks.

This setup allows businesses to run secure, real-time, and scalable transaction flows, reducing failure points and ensuring PCI compliance.

Issuer Processor Architecture on AWS

- AWS Direct Connect & Transit Gateway: Establishes private connections from legacy on-prem systems.

- Network Load Balancer: Routes socket traffic from card networks.

- Tokenization VPC + AWS Payment Cryptography: Handles secure decryption and token validation.

- Authorization VPC with EKS: Hosts containerized app performing business policy checks.

- Amazon DynamoDB & MSK: Stores and streams processed responses.

- Amazon ElastiCache: Delivers sub-millisecond access to frequently accessed tokenized data.

This highly resilient architecture empowers issuing banks to respond to millions of authorization requests in real time, all while maintaining compliance and performance integrity.

Real-World Use Cases and Business Impact

Building a payment processing platform on AWS is not just about tech—it’s about business enablement. Companies can:

- Launch faster: Rapid prototyping with infrastructure-as-code.

- Expand globally: Easily deploy in multiple regions using Availability Zones.

- Optimize marketing: Use tools like Amazon Comprehend and Amazon Personalize for insights and recommendations.

- Ensure compliance: Leverage AWS Config Rules, CloudFormation Guard, and Service Catalog for governance.

Security and Compliance on AWS

Security is paramount in credit card processing. AWS supports PCI DSS compliance and offers:

- Identity & Access Management (IAM): Fine-grained control over access.

- Threat Detection: Via AWS GuardDuty and AWS Security Hub.

- Data Encryption: Both in transit and at rest using KMS and Secrets Manager.

- Network Isolation: With VPC, PrivateLink, and NACLs.

These features help businesses meet the highest security standards in the payments industry.

The Future of Credit Card Payments

As digital payments evolve, so do customer expectations. The ability to issue virtual credit cards instantly, integrate with digital wallets, and offer custom loyalty programs are just a few of the innovations enabled by AWS infrastructure.

According to industry data, credit card usage continues to grow post-pandemic, especially for travel and entertainment. Businesses that adopt modern, cloud-based platforms will gain a competitive edge.

Final Thoughts

If you’re looking to build a secure, scalable, and compliant credit card processing platform, AWS provides all the necessary building blocks. From container orchestration to real-time data streaming, and from encryption services to global infrastructure, AWS can power payment experiences that meet today’s demand and tomorrow’s innovation.

For further assistance or to explore custom architectures tailored to your business needs, reach out to your AWS Account Manager or visit the AWS Financial Services – Payments page.

Discussion