In the first quarter of 2025, the UK job market has shown the clearest signs of strain since the pandemic. Employer payrolls dropped sharply in March, just ahead of the tax rise implemented by Chancellor Rachel Reeves, while wage growth continued at a pace that complicates the Bank of England’s decision-making.

Job Cuts Intensify Ahead of April Tax Shift

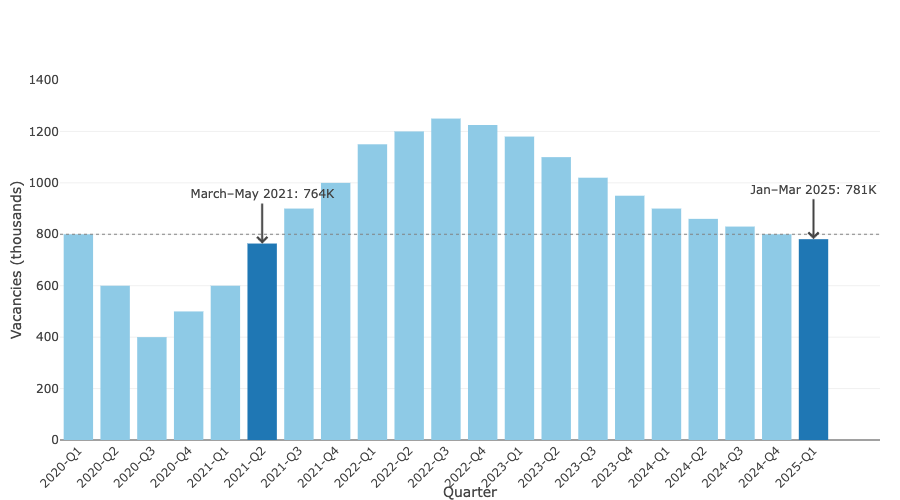

For the first time since the COVID-19 pandemic, job vacancies in the UK fell below pre-2020 levels, according to new data from the Office for National Statistics (ONS). Between January and March 2025, the number of open positions declined steadily, marking a significant turning point for Britain’s post-pandemic labour recovery.

Employers reported a net loss of 78,000 employees in March, the steepest monthly decline since the early days of the pandemic in 2020. The trend reversal is striking, considering that February figures were also revised down—from a previously estimated gain of 21,000 jobs to a loss of 8,000.

“We’re seeing the early effects of tightening fiscal policy,” said Sanjay Raja, Chief UK Economist at Deutsche Bank. “The tax rise has led employers to reassess staffing levels even before it officially took effect.”

Wages Climb—but For How Long?

Despite the job cuts, wage growth remains robust, with average weekly earnings (excluding bonuses) rising by 5.9 percent year-on-year in the three months to February. This was slightly faster than the 5.8 percent pace recorded in January and close to economists’ expectations of 6.0 percent.

Private-sector pay, a key inflationary indicator closely watched by the Bank of England, mirrored the same 5.9 percent annual increase.

However, the outlook is shifting.

“April’s increase in National Insurance Contributions and a 7 percent rise in the National Minimum Wage will likely put downward pressure on hiring,” noted Yael Selfin, Chief Economist at KPMG UK. “We may see wage growth cool in the coming months.”

Bank of England: Between Slack and Sticky Wages

The Monetary Policy Committee (MPC) at the Bank of England is in a precarious position. Investors are currently pricing in a 90 percent chance of a 0.25 percent rate cut in the next MPC meeting on May 8. But with consumer price inflation expected to hover around 2.7 percent in March—still well above the central bank’s 2 percent target—the timing remains uncertain.

“There’s clear emerging slack in the labour market,” Raja added. “But wage stickiness may delay aggressive policy easing.”

Additionally, external pressures are building. The new round of U.S. trade tariffs, pushed forward by President Donald Trump, is forecast to hit global trade flows. This is expected to impact the UK directly through reduced export competitiveness and indirectly via slower global demand.

Is the Official Unemployment Rate Misleading?

The ONS has held the UK’s official unemployment rate at 4.4 percent, but questions about its accuracy are mounting. The agency is currently overhauling its methodology amid suggestions that the true figure may be significantly higher.

“We estimate actual unemployment to be closer to 4.8 or 4.9 percent,” said Gabriella Dickens, G7 Economist at AXA Investment Managers.

This discrepancy may further complicate the BoE’s attempts to assess the true state of the labour market, especially as it relates to domestic inflation pressures.

Looking Ahead: Labour Pain Before Policy Gain?

As the UK economy braces for tighter fiscal conditions and global trade uncertainty, the early-year labour data suggests that businesses are proactively reducing headcount in anticipation of cost hikes.

Whether this leads to a broader economic slowdown or a policy pivot from the BoE will depend on the balance between labour market slack, wage pressures, and consumer inflation in the months to come.

Discussion